Flowing Your Way to Affluence

photo credit: ideogram.ai

When you hear the word “affluent,” especially in the context of a message from a financial advisor, it’s almost certain you think of its most common use:

Affluent (adjective): having an abundance of goods or riches: wealthy.

Did you know that affluent is also a noun? And, no—not one just used to mean “a wealthy person.” In fact, the primary use of “affluent” as a noun is:

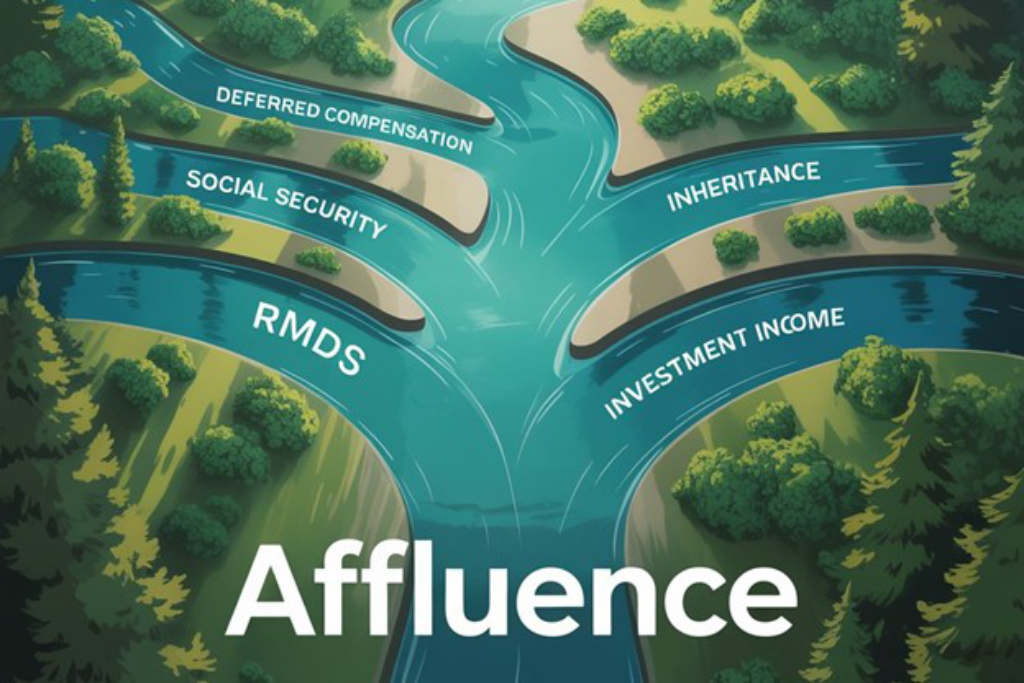

Affluent (noun): a tributary stream; a stream that flows into a larger river or lake.

What does an affluent—a stream—have to do with affluence? Where is the confluence of these concepts?

Many of us can have various streams of income—investments, deferred compensation, social security, inheritance, required minimum distributions—all flowing toward the endpoint of a comfortable, tax-efficient retirement. Income smoothing is a strategy used to keep lifestyle expenses in flow, while minimizing tax impact of withdrawals over time.

In simple terms, the goal of income smoothing is to even out your income year over year to minimize jagged ups and downs—years of extreme high earning or deeper lows.

Take, for example, a seventy-something year old whose income needs are fulfilled without drawing from an IRA. When this client reaches the age of Required Minimum Distributions (RMDs), they will be required to draw from their IRA and pay taxes on the withdrawal, whether they need the money or not. This means that the client could go from a steady lifestyle with $0 in qualified distributions to taking $60,000 from an IRA — a sudden jump, which could result in an unpleasant tax bill— if they haven’t planned ahead. In a case like this, it may make sense to take a $30,000 distribution from the IRA before it is needed, lowering the future tax bracket and smoothing the impact of an eventually required distribution. The goal is to minimize tax bracket variability during your retirement years.

Other potentially beneficial income smoothing strategies to consider include:

- Annual Taxable Income - Be aware of other sources of taxable income when determining distributions from one year to the next. When other sources of income are higher, consider reducing distributions from retirement accounts, if possible.

- Charitable Giving - When Required Minimum Distributions (RMDs) exceed current cash needs, consider giving all or a portion of your RMD directly to a qualified charity. This tax-free withdrawal option is called a Qualified Charitable Distribution (QCD) and is available beginning at age 70 ½ before RMD age.

- Roth Conversions - Another preferred option for excess taxable distributions is a Roth rollover. The income is recognized in the year of the rollover while future growth and distributions will be tax-free from the Roth IRA.

- Using Standard Deduction - Always distribute enough from your retirement accounts to bring your taxable income to at least the amount of the standard deduction, even if you do not need the money. Consider taking enough to reach the top end of the lowest tax bracket as well. Save or invest what you do not need and use it in the future.

- Roth Distributions - If you have Roth retirement assets, you may use distributions from Roth accounts to supplement your cash flow, smoothing your taxable income from one year to the next as well (no taxes paid on Roth qualified withdrawal).

- Spreading Distributions - When anticipating a large purchase, consider attempting to spread the distributions needed to cover the purchase over two or more years, rather than taking a lump sum in one year.

There are several things you can do to regulate the tax impact of significant required minimum distributions (RMDs). Prior to reaching RMD age, drawing dollars from your pre-tax retirement accounts will reduce the amount of the eventual required minimum distribution. Think ahead to what is upstream and how you can start preparing today.

Certainly, one can point to examples of rivers that are anything but smooth—but you’ll likely prefer a metaphorical lazy river to the thrill of whitewater rafting through your financial life in retirement. Income smoothing is just one strategy to help you flow your way to affluence.

To learn more about the confluence of affluence, reach out to Randy Fairfax by email, rfairfax@highlandusa.net, or call 440-808-1500.

Highland Consulting Associates, Inc. was founded in 1993 with the conviction that companies and individuals could be better served with integrity, impartiality, and stewardship. Today, Highland is 100% owned by a team of owner-associates galvanized around this promise: As your Investor Advocates®, we are Client First. Every Opportunity. Every Interaction.

Highland Consulting Associates, Inc. is a registered investment adviser. Information presented is for educational purposes only and is not intended to make an offer of solicitation for the sale or purchase of specific securities, investments, or investment strategies. Investments involve risk and unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Past performance is not indicative of future performance.