Return Forecasting Isn’t Prediction — It’s Disciplined Preparation

Photo credit: Unsplash

Long‑term investors don’t need a crystal ball — they need a framework. Forecasting returns is not an exercise in predicting the next market swing, but in understanding the structural forces that reliably drive outcomes over full cycles. By focusing on observable inputs like income, real earnings growth, inflation, and credit losses — and by deliberately excluding unforecastable variables such as valuation shifts or interest‑rate timing — investors can approach an uncertain future with discipline rather than guesswork. This is the foundation of Highland’s capital‑market expectations: a transparent, data‑driven methodology designed to help institutions prepare, not predict.

Every year, long‑term investors confront the same essential challenge: What returns can we reasonably expect from capital markets in the years ahead? While the future is inherently uncertain, institutions cannot wait for clarity before making decisions. Budgets must be set. Spending policies must be calibrated. Actuarial assumptions must be updated. And portfolios must be constructed to balance opportunity with risk.

At Highland, we view capital market expectations as a strategic tool—grounded in observable data, transparent in methodology, and designed to help investors navigate uncertainty with discipline and confidence.

Why Return Expectations Matter: Discipline > Prediction

Return expectations play a central role in how institutions plan for the future. Decisions about the future usually occur before clarity arrives. Nonprofits and foundations depend on investment projections to determine what level of spending they can sustain over time without compromising their missions. Defined benefit plans rely on these same assumptions in their actuarial valuations and financial statements, where even small shifts in expected returns can meaningfully affect funding status. Across the broader institutional landscape, every investor benefits from a clear understanding of where returns come from and the risks involved, allowing them to build portfolios that align with their objectives, constraints, and long‑term responsibilities.

Setting expectations is not about predicting the next market move. It is about understanding the structural forces that drive returns over full cycles.

How We Build Return Expectations

All asset classes generate returns from two fundamental sources:

- Income: The cash payments investors receive—dividends, interest, and share repurchases.

- Price Appreciation: The change in the market’s valuation of future cash flows.

Inflation influences both components. Because returns can be expressed in nominal terms (including inflation) or real terms (after inflation), inflation expectations are a critical input in any forward‑looking model.

Equities: Cashflows, Growth, and Valuation

Cashflows: Dividends and Buybacks

Dividend payments have become a smaller share of total equity returns over time, as price appreciation has outpaced cash distributions. Share repurchases have grown more common, but they are less predictable and harder to model.

Source: Bloomberg, S&P 500 Index

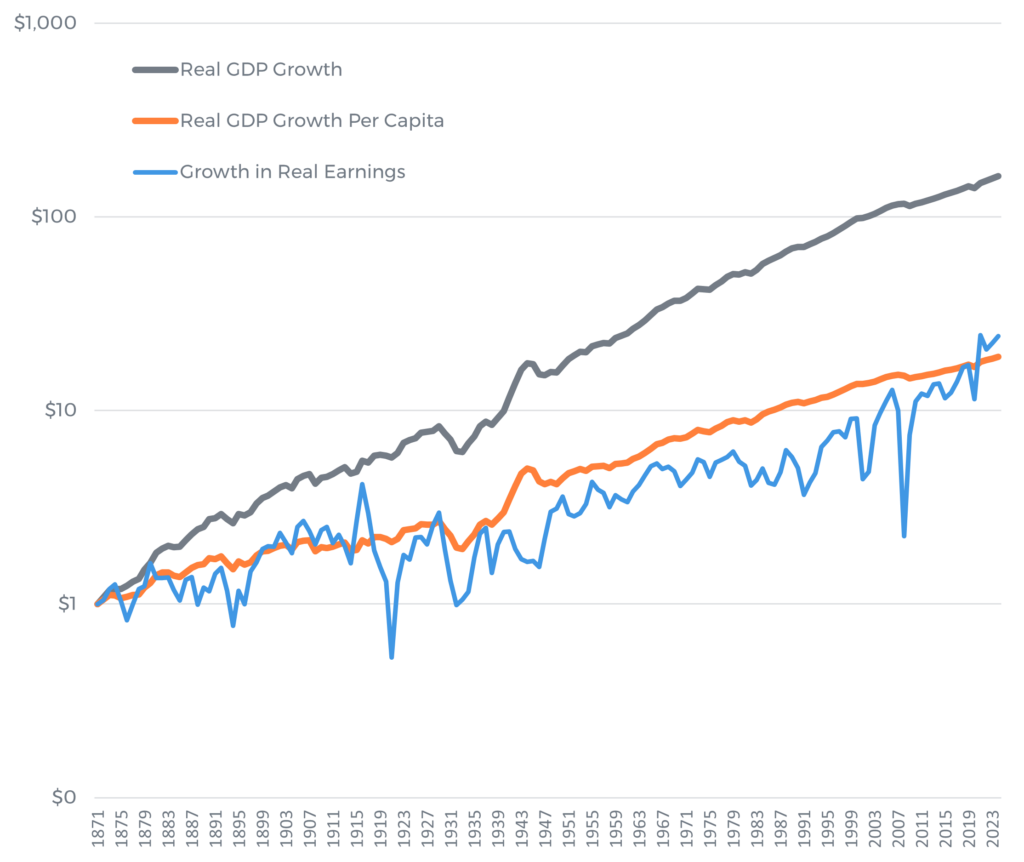

Growth: Real Earnings Power

Real earnings growth—not GDP growth—is the engine of long‑term equity appreciation. Public companies do not capture the full breadth of economic activity, especially in periods of rapid private‑sector expansion. Over long horizons, cumulative real earnings growth tends to track real GDP per capita, a more stable and representative measure.

Sources: Samuel H. Williamson, What Was the U.S. GDP Then? MeasuringWorth, 2026. Robert J. Shiller, Stock Market Data Used in “Irrational Exuberance” (Princeton University Press, 2000, 2005, 2015; updated).

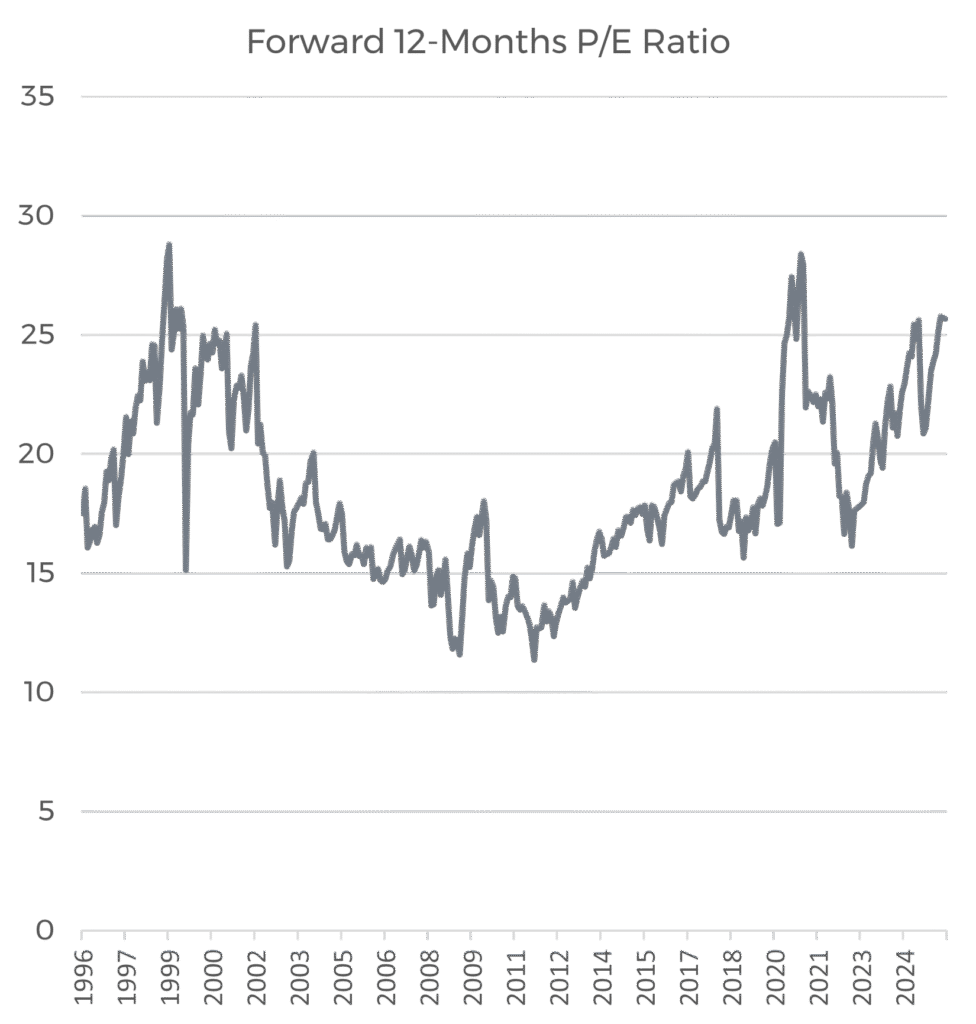

Valuation: The Unforecastable Variable

Valuation changes—shifts in the multiple investors are willing to pay for earnings—can dramatically influence short‑term returns. But they are not reliably forecastable. Because valuation swings are cyclical and often extreme, Highland excludes valuation changes from forward projections.

Source: Bloomberg; S&P 500 Index.

Bonds: Income First, Price Second

Income: Yield as the Anchor

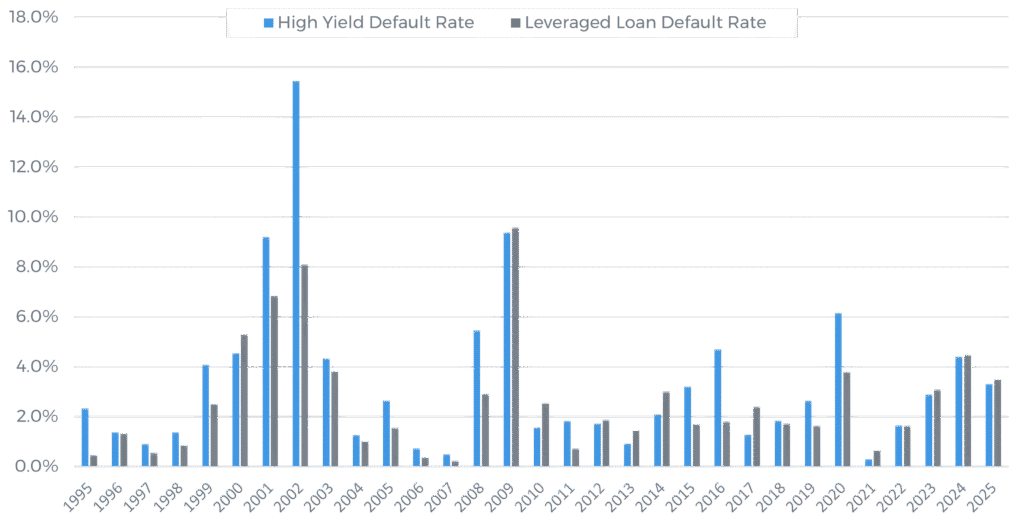

Bond yields incorporate expectations for inflation, credit risk, and interest rates. For investment‑grade bonds, yields provide a strong baseline for forward returns. For high‑yield and emerging‑market debt, expected credit losses must be deducted from yield to estimate income return.

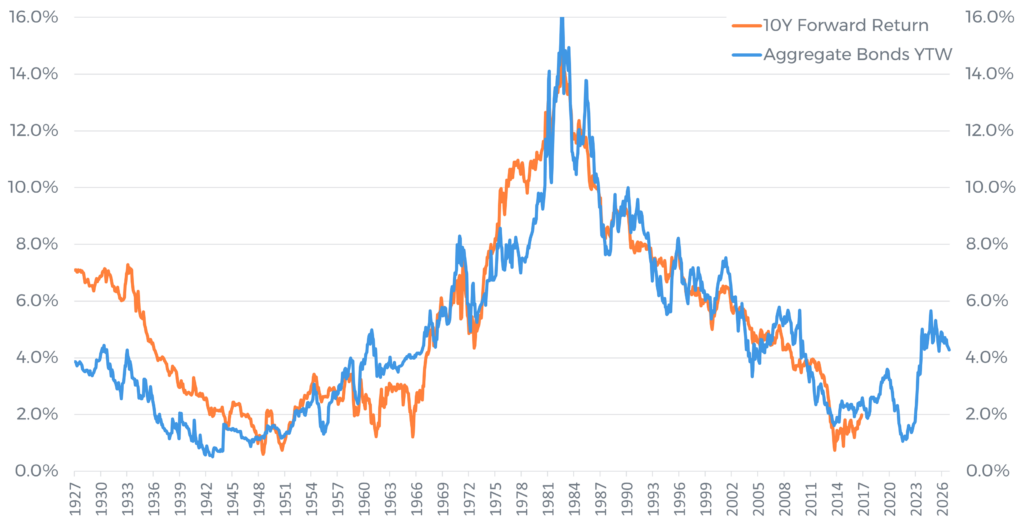

Price: The Interest Rate Effect

Bond prices move inversely with interest rates. Longer‑maturity bonds are more sensitive to rate changes, while shorter‑maturity bonds are less affected. But like equity valuations, interest rate movements are not structurally predictable. Over long horizons, price effects tend to wash out, leaving yield as the dominant driver of returns.

Sources: S&P; Fitch; UBS; Aristotle Pacific Capital

Sources: Bloomberg; Morningstar. Aggregate Bonds represented by the Bloomberg U.S. Aggregate Bond Index

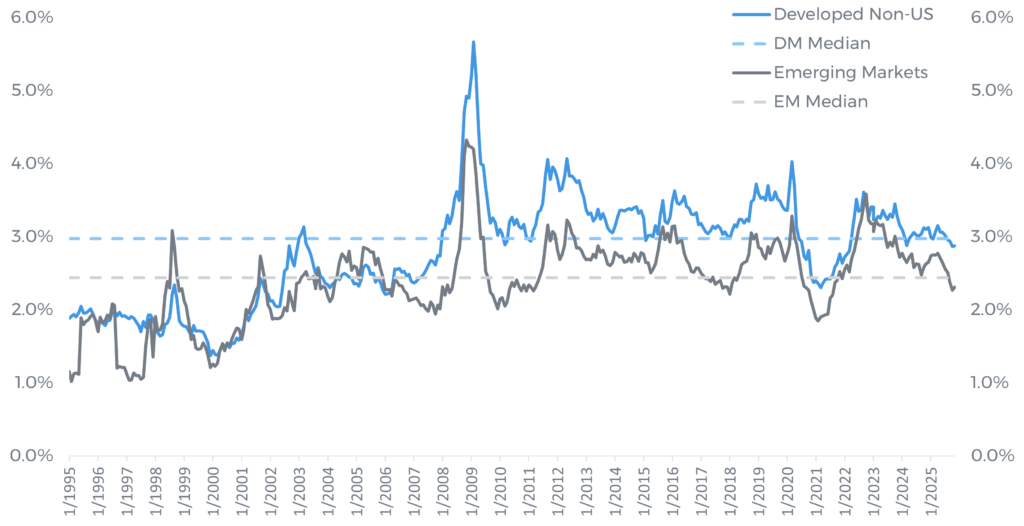

Global Markets: Additional Layers of Complexity

International markets share the same fundamental return components—income and price—but with important distinctions:

- Developed markets have typically grown more slowly than the U.S.

- Emerging markets offer higher growth potential as their economies progress.

- Dividend yields abroad are generally higher than in the U.S.

- Interest rate regimes vary widely, creating different opportunities in global fixed income.

- Currency effects can meaningfully influence returns for U.S.‑based investors, but FX forecasting is as uncertain as predicting valuations or interest rates.

Source: Bloomberg; 10-year government bond

Source: Bloomberg; Developed Non-US and Emerging Markets are represented by MSCI EAFE and MSCI Emerging Markets Index, respectively

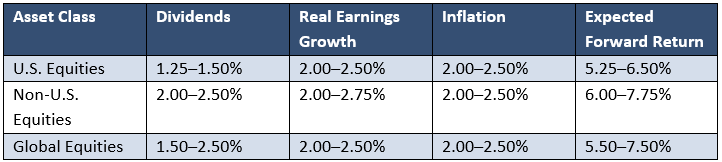

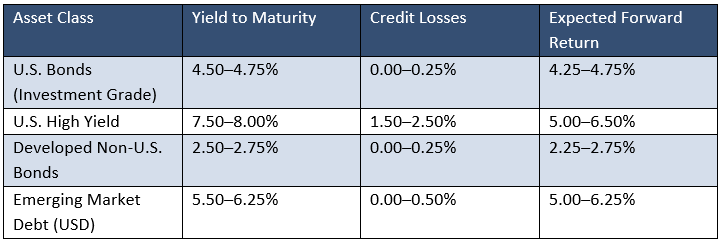

2026 Forward Return Expectations

Below are Highland’s data‑driven return expectations based on 2026 inputs. These ranges reflect long‑term structural drivers, not short‑term market views.*

Equities

Fixed Income

*Expectations should not be used to inform security decisions without consultation of an investment or financial advisor.

The Highland Perspective

Forecasting returns is not about predicting the future, it is about preparing for it. By grounding expectations in observable drivers of income and growth, and by avoiding unreliable assumptions about valuations or interest rates, investors can build portfolios that are durable, disciplined, and aligned with long‑term objectives.

In a world where uncertainty is constant, clarity becomes a strategic advantage. Highland remains committed to helping institutions navigate that uncertainty with data‑driven insight and steady guidance.

Highland Consulting Associates, Inc. was founded in 1993 with the conviction that companies and individuals could be better served with integrity, impartiality, and stewardship. Today, Highland is 100% owned by a team of owner-associates galvanized around this promise: As your Investor Advocates®, we are Client First. Every Opportunity. Every Interaction.

Highland Consulting Associates, Inc. is a registered investment adviser. Information presented is for educational purposes only and is not intended to make an offer of solicitation for the sale or purchase of specific securities, investments, or investment strategies. Investments involve risk and unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Past performance is not indicative of future performance.